Formula 1 (FWONK) - Shifting Gears

Formula 1 (FWONK) - Shifting Gears

Thoughts on the Formula 1 franchise and Company Structure. If you like the article please subscribe - I plan to do an in-depth analysis on a company every month.

It is no secret that I am a big fan of entertainment brands; in my previous note on Nintendo (link), I’ve talked about the strength of the Nintendo franchise and how the market often undervalues some brands compared to others. In this note, I’ll talk a bit about the Formula One franchise and my thoughts on the future prospects of the company.

History:

With roots dating back to the 1920s but officially formed in the 1950s, Formula one has steadily grown to become one of the most popular motorsports around the world. Over the years, fans were drawn to technological innovation that F1 teams employed to achieve the fastest times around the grid.

Despite its long history, the sport only started to formalise under Bernie Ecclestone (originally an F1 team owner) in the 1970s. Original discussions around organising races were anything but organised; there were many separate negotiations with separate parties; F1 teams individually would have to negotiate with the regulators (FIA/FISA) as well as broadcasters, promoters, advertisers and sponsors leading up to a race. Frequent disagreement arose between the team around the size of the pay-out and who splits the bill. Ultimately, this led to several races being cancelled.

Things started to change when Bernie started to organise the F1 teams under one umbrella (now called the Formula One group). This enabled the teams to have more bargaining power in negotiations – whereas negotiations historically were every team for themselves, Bernie was able to organise them and settle negotiations as a collective. In the 80’s, the first Concorde agreement was signed with scheduled re-negotiations every couple of years - this guaranteed the split for each team from each race (from broadcasting revenue and price money) and in return, all teams would have to attend each race.

Over the years, stakes in the F1 group were sold in the private markets to PE firms such as CVC. Bernie still retained control over the company however, as characteristic of most PE investments, the resulting years of underinvestment and short-termism lead to the sport’s eventual decline in viewership numbers.

Enter Liberty:

In 2016, the sports franchise changed hands once again with John Malone (the widely known “Cable Cowboy” and former CEO of TCI) and Liberty Media purchasing the F1 parent company. As an aftermath of the transaction (and a common Malone strategy), Liberty issued a tracking stock that provided investors with exposure to the F1 franchise along with other eclectic mix of assets.

If anyone doesn’t know of Malone, I would recommend reading The Cable Cowboy (LINK). In short, Malone pioneered telecom investing through focusing on minimising tax leakage, maximising free cash flow per share and judicious reinvestment of free cash flow ultimately leading to the sale of his company TCI to AT&T for $48bn in 1998. Afterwards, he has dabbled with investing in the TMT space through his Liberty Media vehicle and generate outsized returns as a result.

Whereas Malone typically invests across the TMT space, the similarity between all his investments is the ensuing complexity and structure that befuddle most investors. Despite this, I believe the story around FWONK is relatively clear – the company has historically been mismanaged under Bernie and PE firms leading to its stagnant financial performance and poor viewership metrics. New management (Chase Carey and now Stefano Domenicali) instilled by Malone and introduction of the right incentives should help steer the company to continued long term growth.

FWONK holds stakes in a number of public equity holdings such as the Liberty Braves and AT&T however the crown jewel is undoubtedly the F1 franchise itself.

The reason why FWONK is so interesting to me is that it is possibly the only opportunity for public market investors to invest into a sports franchise. Many other publicly listed companies provide exposure to a segment of certain sports franchises; however the performance of a team within their respective sport often influences the economics of the stock to a large degree and, in most instances, teams are run for emotional sentimental reasons rather than for financial ones. An example of this would be Manchester United’s flat performance since inception after the retirement of the legendary football manager Sir Alex Ferguson.

F1 controls the commercial IP rights of the sport through a lease agreement with the FIA (the motorsport regulator) lasting until 2110. As a result, F1 controls all programming, merchandising, licensing, advertising, and sponsorship rights as well as helping organise new F1 venues around the world.

The underlying economics of the business are phenomenal – revenue streams are predictable with locked in contracts spanning 3 -10 years in duration with built-in fee escalators. The franchise requires little capital expenditure costs resulting in high free cash flow conversion and margins. The company is structured in a way that maximises tax efficiency (a trademark of any John Malone investment) which has resulted in a relatively underfollowed opportunity outside of traditional indexes.

There is leverage in the company with roughly 5x net debt/EBITDA (this has fallen from 8x when Malone acquired the company). However, with vast majority of the debt maturing in 2023 and onwards, solvency risk is low. Vast majority of the cash flow will either be used for paying off the debt, making strategic acquisitions or reinvesting into organic growth.

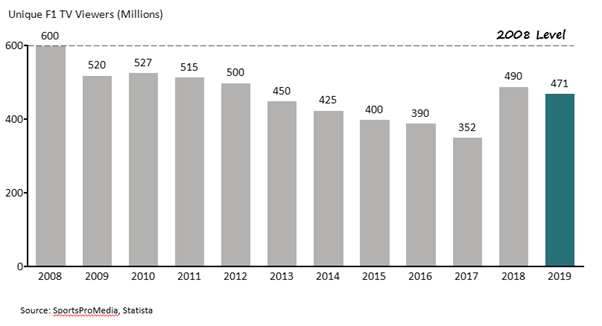

As seen in their prospectus, F1 still is able to generate some of the highest viewership and attendance numbers out of any sport. Yet monetization of those viewers is still low. This is F1’s decision to handicap their reach through signing Pay-to-View broadcasting contracts rather than Free-to-view TV. However, Bernie’s scandals didn’t help F1’s family friendly image.

Revenue streams:

F1 revenue streams can be broken down into 4 segments:

Race Promotion Fees – fees paid by venues to host the races.

Broadcasting Fees – earned from licensing the right to broadcast the events on TV or Online

Advertising Fees - paid by sponsors to advertise within the races.

Other revenue – revenue generated from ancillary services, F2/3 as well as their OTT subscription service F1 TV.

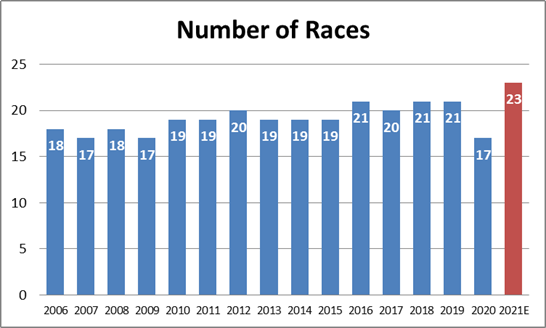

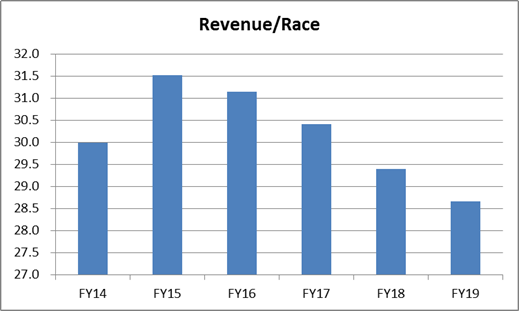

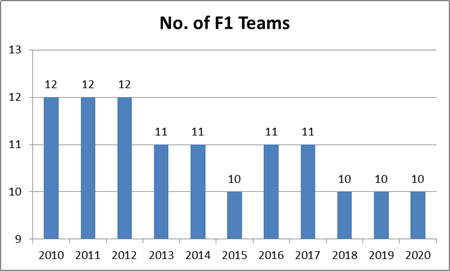

Race Promotion fees are simple enough: the more F1 venues you organise per season, the more revenue you generate. Venues typically are arranged a couple years in advance and contracts between F1 and the racing venues last for 3 – 5 years with options to extend. Races have been gradually trending up over the past 15 years. 2020 season was originally scheduled to include 22 races however was cut to 17 as a result of COVID. Revenue per race has remained steady over the past 5 years at c.$30m per race and I expect this to continue as more races are added in future seasons (Formula 1 have recently announced a 23 race season for 2021) There is an agreement between FIA and F1 to place a soft-cap of 25 races within a season however I could see this being lifted in the foreseeable future given that both parties stand to benefit from more races (more fees for both parties!).

More venues mean more opportunities to attract local crowds and increase the geographical split of their revenue. Although the company does not disclose revenue split by geography, the majority of the F1 audience is situated within Europe (48% of the 2019 races and 76% of 2020 races were situated within Europe). Opportunities to expand viewership numbers within the US and China would provide a huge tailwind to future revenues.

“[The US is] under-viewed, under-monetised, under-everything… I don’t think that gets solved in a week but I think that’s an interesting long-term opportunity” Greg Maffei, Liberty Media CEO

Despite hosting grand prix in the US every year since 2012, Formula 1 is still the third most popular motorsport in the region (behind Indycar and NASCAR). US viewership numbers are showing promising growthover the past couple years. Clearly there is a lot of focus by Liberty Media to expand into the US globally and improving numbers will help with future sponsorship and broadcasting negotiation contracts. A current overhang to watch is F1’s renewal negotiations with Circuit of The Americas (where they host the US Grand Prix) in 2021 – securing the renewal will be pivotal in attracting a larger US fanbase.

Viewership numbers within emerging markets such as China and Brazil are also growing year on year (Nielsen estimates that China and Brazil have the largest F1 fan bases globally) however monetization in these regions is expected to be low.

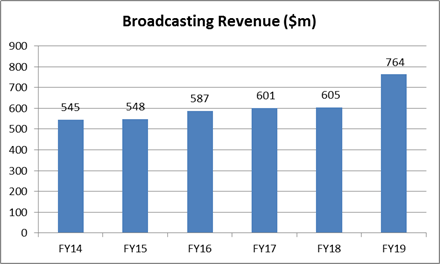

Broadcasting fees have grown at 7% CAGR over the past five years through a combination of negotiated yearly fee increases (3-5% every year) and contract renewals with TV and online broadcasters. Contracts vary in duration depending on different regions; in any one year, there are always contracts to be renewed however the large step-up in revenue typically occurs every 3 years. The last 2 resign multiples occurred at 1.07x and 1.26x (compared to the previous contracts average annual payment).

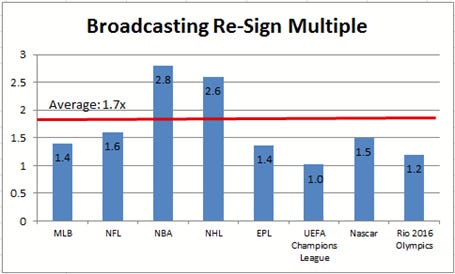

When you compare resign multiples against other sports franchises, you will see that huge disparity between different sports. Upon further examination, we can see that US sports franchises typically resign broadcasting contracts at higher values than their previous contracts. Given that live sport is such a pivotal part of the cable’s value proposition vs. digital content providers, re-sign multiples should potentially increase for the foreseeable future as more TV stations try to differentiate themselves.

As F1 gains a larger dedicated following within the US, I could see broadcasting multiples converging to similar US franchises. Currently, Formula 1’s 1.26x resign multiple is at the lower end of this scale but should meaningfully increase to that of NASCAR’s as they continue to gain popularity within the US. This is despite NASCAR’s continuously falling viewership base over the last 20 years.

Advertising Revenue:

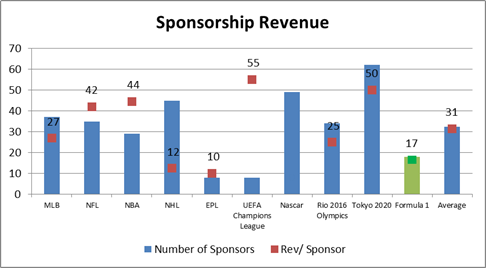

Soon after the acquisition, Liberty Media set about doubling the headcount of Formula 1 headquarters to 150; most of the hires were concentrated within their sponsorship team. Sponsorship metrics screen poorly against peers on most metrics and still require further investment and time to develop an attractive platform for advertisers.

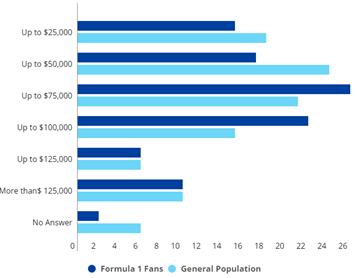

The recent sponsorship deal with Saudi Aramco, announced this year, suggests that the F1 platform may be an attractive proposition for brand visibility in the emerging markets (especially given that the F1 audience skews more towards a wealthier demographic). With possible future growth in viewership, the sponsorship opportunities should growth commensurately along with revenue per sponsor.

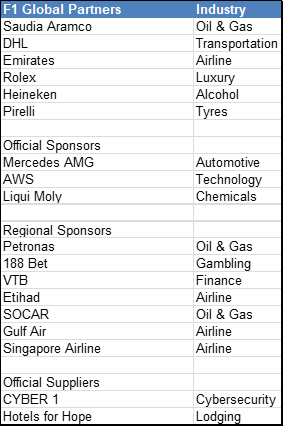

Looking at the list of F1 sponsors, there is potential for sponsorships across a wide variety of industries such as Finance, Consumer staples to Telecommunications and Technology.

Other revenue sources:

Making up 18% of total revenue, there are a lot of activities bundled together under this segment. The company does not breakdown revenue sources within this segment which doesn’t exactly help with forecasting or analysis. Nonetheless, there are promising segments of growth to be aware of.

Greg Maffei has frequently alluded to increasing investment into digital value-add services. Whilst these ventures may never generate significant revenue to move the needle by themselves, they should increase the visibility of the sport worldwide.

A recent partnership with Netflix for their “Drive to Survive” series is already the 4th most popular documentary on Netflix. Whilst unlikely to be profitable, the venture will hopefully help attract a different audience base, from Netflix’s 195m viewer platform, to the sport. Given the success of the series, there are plans to create a 3rd season to the show.

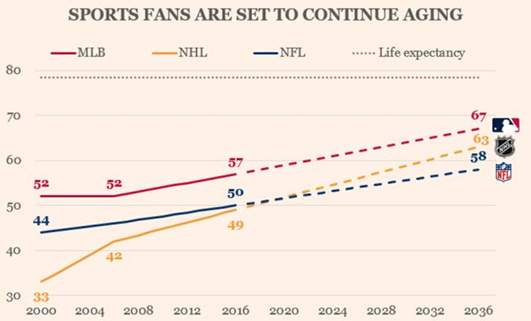

The introduction of the E-sports E-series (the official F1 E-sports league) also provides an avenue for F1 to attract a younger audience (a headwind that is faced by many sports franchises worldwide). With nearly 80% of E-sports viewers under 34, there is a plausible chance that many of the viewers express an interest in F1 itself and convert into becoming an F1 viewer. The initial signs are encouraging; recent surveys performed on F1 fans have shown growth in fan base within the 16-24 age range.

F1 have also released their OTT service called F1 TV. For $26.99/year, the subscription service provides alternative angles, real time data analytics and archived footage of historical races which will likely attract the die-hard formula 1 fan. Frank Arthofer, F1’s Director of Digital and Licensing, estimates that there is a potential 5m addressable viewer base that will be attracted to this service. If those assumptions are correct, this could lead to $135m incremental revenue that will largely flow down to the bottom line. The introduction of the OTT service did throw a spanner in the works in broadcasting negotiations with NBC Sport resulting ESPN picking up F1 coverage for free.

The introduction of this service likely scuppered many other broadcasting negotiations leading to a temporarily depressed resign multiple last year. Clearly management have confidence that F1 TV will improve the franchise in the long run. With current sell side estimates of 200k – 300k subscribers on the OTT service, the data however suggests otherwise.

What attracts viewers on the margin?

“If I was watching today [as a fan], I would most likely do the same and watch the highlights…” Lewis Hamilton, 7-time Formula 1 winner

Really, the heart of the debate around the future success of Formula 1 lies not in the financials of the business but in the intrinsic qualities of the sport itself; is the sport enjoyable to watch?

There have been frequent complaints of F1 by fans over the years over a wide variety of factors however bottom line is that the main limiting factor behind attracting new viewers is the lack of competitiveness within the sport. With only 3 different winning drivers and 2 different winning teams in the last 10 years, winners have gotten more predictable over the years.

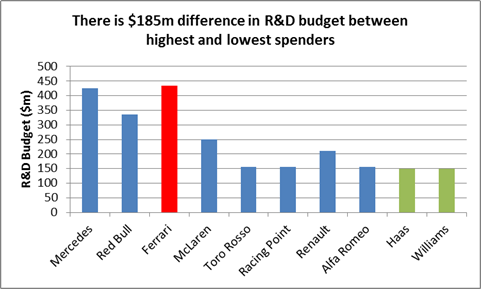

With greater and greater investment pumped in the R&D by the larger teams (used as a marketing branch by their corporate owners), the disparity between the winners and losers has widened over time. Couple this with the fact that most F1 teams are loss making or breakeven at best, being owned by a corporation seems to be a prerequisite for success on the grid.

Why have things changed?

With the Concorde agreement that has been signed this year, the overhang surrounding contract negotiations has been lifted providing greater visibility for the next 5 years (until the next Concorde agreement is scheduled to be negotiated). Whilst most of the terms of the new agreement have yet to publicly revealed, what can be gleaned from Maffei’s quotes suggest steps have been taken to make the sport more competitive and appealing to viewers.

Unanimity is no longer required between the 10 F1 teams to push things through major amendments to the sport (they now only require the agreement of 8 teams). As a result, there is no longer the risk of a team blocking beneficial changes to the sport purely for self-interest.

Formula 1 has followed the footsteps of the NBA/NHL/NFL through the introduction of budget caps. This spending cap only includes expenditure related improving car performance. With a $145m spending cap being introduced in 2021 and tapering down to $135m by 2023, future winning teams will determined by skill of the driver rather than the amount of money they put into R&D. Penalties, ranging from points deduction to exclusion from the World Champions, will deter any breaching of the rules.

A new committee (named “The Working Group”) was created to identify and prevent exploitation of loopholes that may occur after introduction of the new rules. Historically, there have been multiple occurrences of F1 teams exploiting these loopholes to gain an aerodynamic edge within the race (Brawn GP famously won the 2009 World Championship through these practices).

Race weekends will be more condensed from four days to three days providing a better viewing experience.

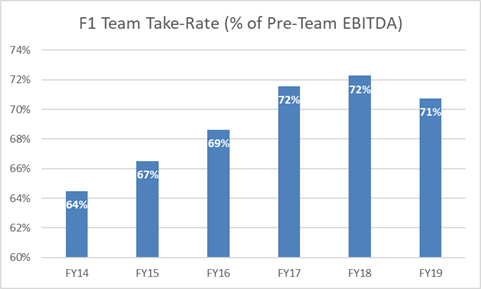

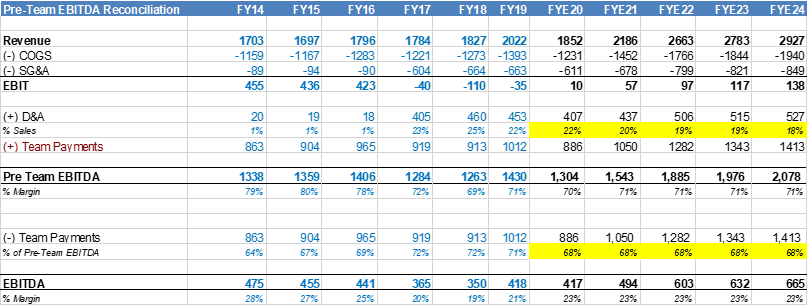

I’m unsure how the new Concorde agreement will affect F1 teams take rate from FWONK (historically, teams have received around 65% of pre-team EBITDA but this has gradually increased the company have been bought). The most pressing issue affecting FWONK’s margins is whether the take rate will increase in the future. At a first glance, the negotiations seem to negatively impact the F1 teams however the changes should be conducive in attracting new fans to the sport. Over time, this should result in higher broadcasting, promotional and advertising revenue for Formula 1 and flow down the competing teams. The elephant in the room is would the F1 teams be willing to take a smaller chunk of a growing pie or a large chunk of a potentially shrinking pie. My money would be on the former.

Recent Events:

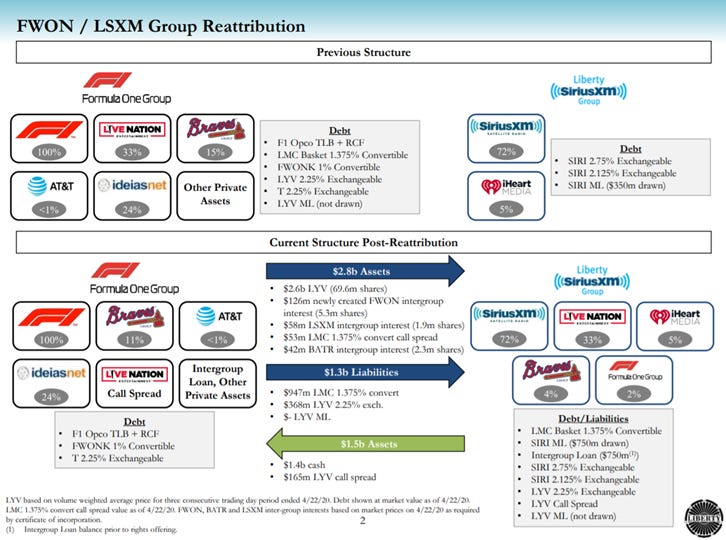

With the recent interparty transaction (outlined below), some of the complexity around the FWONK structure (the Live Entertainment Stake, Convertible debt etc) has been removed play on Formula 1.

I won’t dig down too deep into the weeds, but Liberty Formula One essentially sold some out-of-the-money naked calls on Liberty Sirius Shares. The calls became in-the-money during COVID so Malone and Co. had to undergo this transaction to cover those calls. Some of the assets within Liberty Media have been rejigged to cover the call options.

Recently, on the 2020 Liberty Investor Meeting, the company has also announced that they were launching a SPAC (ticker: LMACU). The company will acquire $250m stake (out of an expected $500m raise) and attribute it under the FWONK vehicle. The SPAC is expected to target private TMT mid-caps; valuations in that space are high which could create some difficulty but there is some additional upside optionality here provided they make a good transaction.

In terms of potential targets, I believe the Indycar franchise would make sense from Malone’s point of view – there are potential synergies around building up their OTT value proposition (and hopefully pricing power) and it would provide greater power when it comes to contract negotiations with US broadcasters. Liberty’s expertise in ex-US broadcasting will help extend the appeal of Indycar overseas.

"People who have done a great job, like WWE, have a huge amount of content which isn't available on a linear feed so you have more tonnage to put on the Over The Top product… We are never going to have that breadth so that inherently limits some of our upside.” Greg Maffei

Liberty have been making minority investments in Indycar so there clearly is some interest there. However, given the likely size of the transaction, Liberty would only be able to take a minority stake in the franchise. NASCAR has been floated before as an option with Liberty clearly open to owning a stake.

For Liberty Media and FWONK investors, the SPAC will provide a ton of optionality that has yet to be properly valued by the market. All eyes will be on what they will likely buy.

Valuation:

Now let’s see how the valuation stacks up to the story:

Promotion revenue is driven by number of races per season and revenue generated per race. I project revenue per race to stay constant for the next 5 years (I have no conviction that revenue per race will meaningfully move in either direction). 17 and 23 races are scheduled for this year and next year respectively. I suspect races will increase to 25 by 2024 (the upper limit before Formula One needs to get authorization from the FIA).

For Broadcasting revenue, I assume an annual fee escalator of 2% ever year (this is less than the 3-5% stated by management). I believe resign multiple will increase when major negotiations take place in 2022 – this is because there is no longer the overhang of the F1 OTT release negatively affecting discussions. As such, my projected resign multiple is on par with NASCAR’s historical multiples.

Advertising revenue should meaningfully increase as more sponsors join the F1 platform and there is moderate increase in revenue/sponsor. Hopefully, the changes in the Concorde agreement should increase the competitiveness of the sport and attract a larger fanbase. With growth in viewers, this will encourage more advertisers to partner with F1 as well as an increase in revenue per sponsor.

Since management do not breakdown Other Revenue in more detail, it is hard to project what it will be in the future. I believe that F1 OTT will attract up to 2m viewers by 2024 creating an incremental revenue increase of $47m. This is still below F1 management’s projections of 5m subscribers.

Currently, FWONK trades at c.24x FYE21 EBITDA. The only remotely comparable public company is World Wrestling Entertainment (WWE) which has historically traded at around 20x EV/EBITDA over the past 5 years. I would argue that Formula 1 should trade at a premium to WWE due to greater reach, higher EBITDA margins and better management (someday I will write about Vince McMahon’s mismanagement of WWE). However, due to conservativism, I will stick to 20x EV/EBITDA. Applying a 20x multiple of my estimates of FYE24 EBITDA provides me an estimate of FWONK’s valuation in five years’ time.

* For the value of the LYV call spread, I have assumed it will return the maximum amount (which occurs if LYV shares trade over $47.74).

Adding all my stakes together and subtracting away net debt, the upside on the company doesn’t look particularly attractive. All in all, even looking forward five years, FWONK looks to be fairly valued. There have been rumours that Liberty are looking to sell the asset on – I think it would be unlikely right now but given the amount of interest from PE firms on sports asset and the valuations these deals are occurring at, it wouldn’t surprise me if Malone & Liberty sold it off at the right price.

Although FWONK is unlikely to generate attractive returns over the next five years, given the active involvement by private investors, I will likely be keeping an eye out on this space…

Potential Risks to look out for:

- US grand prix negotiations in 2021

- Resign multiples of broadcasting contracts for other sports. NHL and NFL both have broadcasting rights deal that expire in 2021 so it will be interesting to see what resign multiple are assigned to their new contracts. Any potential signs of a downward re-rating could affect F1’s future broadcasting revenues.

- Number of races to announced for the 2022 season.

If you liked this analysis and want to get reminders on my next analysis, feel free to subscribe. I plan to release a deep dive on a company every month.